The cedi/dollar exchange rate as of last Tuesday stood at GHC5.65 per dollar

The cedi/dollar exchange rate as of last Tuesday stood at GHC5.65 per dollar

Here’s my take on the plunging cedi, the causes, implications for growth, and what to do about it. It’s based on just 5 graphs.

Note that most of the graphs start from 2008 or 2009 and end in 2018 because it is the period with the most consistent data (it has nothing to do with political periodization!). A review of budgets dating back to 1965, when the IMF was first invited to Ghana to save us from fiscal profligacy, shows that the patterns were generally the same.

Where consistent data was available for longer periods, I used them, but keep your eyes on the sparrow….

Graph 1: Compared to three regional currencies – Nigerian naira, Kenyan shilling, and South African rand – the cedi appears to be an inherently weak currency, no matter which government is in power. The lesson: Never politicise the cedi. It might come back to haunt you. (The data is up to 2000, but in fact it is not much different up to at least 1990.)

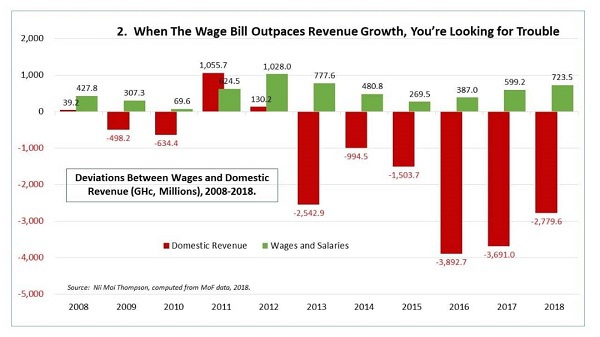

Graph 2: Government may account for only about 6.0 percent of the labour force, but it is the single largest employer and spender in the economy, pathologically inefficient yet having an elephantine appetite. Last year, it pumped an average of GH¢1.84 billion per month into the economy in the form of wages and goods and services (such as the money that goes into buying all those four-wheel drives and the imported fuel to run them). Wages alone accounted for GH¢1.51 billion. In 2019, it is expected to spend GH¢2.15 billion, a 17% increase, far higher than the projected inflation of 8.0%.

Now, all that money must buy something but we hardly produce anything, down to tooth picks. The only option is to buy imports, including used underwear and vehicles condemned as unroadworthy in their home countries. The result? Pressure on the cedi. Macroeconomic theory predicts such an outcome and our experience confirms it.

Meanwhile, government revenue has consistently fallen short of target in all but three of the 11 years. This is a recipe for inflation and exchange rate disaster.

Notice that the wage bill spikes every election year, and we take two years to work it down. It happened in 2009 and 2013. Not so 2017. Instead, we went on a spending spree, creating 44 new districts and 6 news regions in two years and splurging on a range of non-productive manifesto promises like paying trainee allowances and establishing NABCO. With a declining economic growth rate (from 8.1% in 2017 to a projected 5.8% in 2021), revenue shortfalls are likely to grow bigger and continued expansion in government spending will only feed demand for even more imports, contributing to further weakening of the cedi.

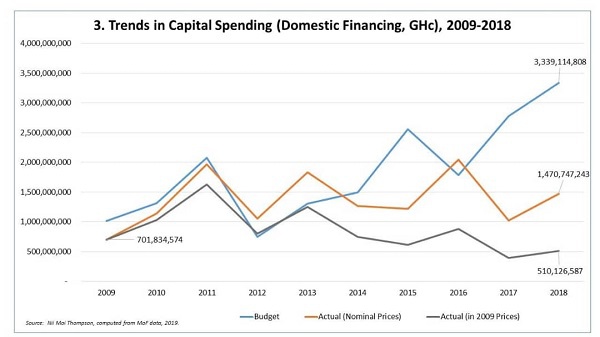

Graph 3: More money for consumption means less for infrastructure development, which is needed to drive economic growth, including exports, to strengthen the cedi. The pattern of infrastructure is like a drunk trying to get home, zip-zagging. It shows a country without a long-term plan of where it wants to be, literally staggering its way through life as it spends more on current consumption and less on growth. The graph shows that except for three years, actual government expenditure (known as “domestic financing” to distinguish it from “foreign finance”) was considerably lower than what was budgeted for. Worse, inflation consistently ate into those allocations.

Hence, although the actual expenditure for 2018 was about GH¢1.5 billion cedis (compared to a budget of GH¢3.34 billion), once adjusted for inflation using 2009 prices, it was actually worth GH¢510.13 million, 27.0% lower than the GH¢701.8 million allocated for infrastructure in 2009. This, in a sense, explains why our infrastructure stock is decrepit and decaying. And I have not even adjusted for corruption, which would reduce the value further.

Graph 4: This graph shows our dangerous dependence on cocoa to support our import-dependent lifestyles. The official data shows that we export oil, gold, cocoa, and other marginal products. In reality, very little of the oil and gold money actually finds its way back into our economy, and so cocoa remains our sole salvation, since 1904, when it took over from palm oil as the leading cash crop. We, therefore, depend on “cocoa syndicated loans”, which come in only once a year to support the cedi, leaving us with no steady sources of export revenue for the rest of the year.

And even then, the highest loan so far was US$2.0 billion (in 2011/2012), when our population was 25.4 million. In 2018, when the population was nearly 30 million, the loan was only US$1.3 billion, which, once adjusted for inflation, was worth only US$1.1 billion. This is one of the structural causes of the inherent weakness of the cedi: The near-sole dependence on cocoa to finance the gargantuan import bills of a growing population.

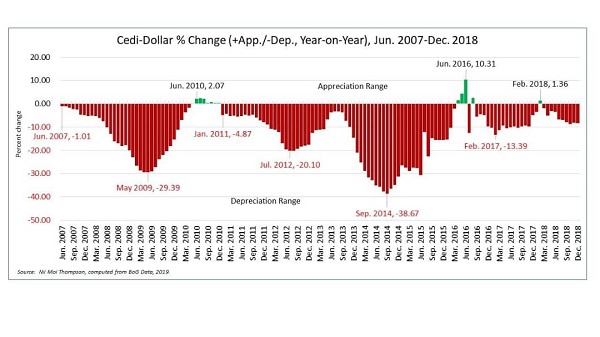

Graph 5: Graph 5 shows trends in the cedi since redenomination in June 2007. Even as the cedi was being born again in June 2007, it was losing its value against the US dollar (1.01% year-on-year). Indeed, the depreciation continued until it peaked at 29.4% in May 2009 and then began to recede. In June 2010, the cedi appreciated for the first time since redenomination to 2.1% against the dollar. The story of this remarkable turnaround is worth stating here briefly: The governor of Bank of Ghana then (a former economics lecturer, deputy finance minister, member of the bank’s board as deputy minister, and hence intimately familiar with the harm reckless government can do in the form of rising inflation and currency depreciation) insisted that the bank would not allow the government to spend even one cedi more than what it was entitled to.

This, it is said, led to major clashes with the finance minister, but the governor stood his ground, and it paid off. In June 2010, inflation fell below 10.0% and by July 2011 it was down to 8.4%, the first time the rate had fallen below 9.0% since 1970, when it was 3.0%. This stability on the inflation front contributed to the continued stability of the cedi against the US dollar for the rest of 2010. Impending-election related expenditures and other acts of fiscal indiscipline in 2011 and 2012 undermined that stability and by July 2012, the cedi had lost 20.1% of its value against the dollar. It firmed up somewhat in 2013, but by 2014 the bottom had fallen out. The continued contraction in economic activity (thanks to dumsor) and a number of policy missteps by the central bank pushed the depreciation to a record 38.7% in September 2014.

The rest, as they say, is history.

So, yes, we need structural transformation and increased exports, etc. But until the government develops and maintains fiscal discipline, we will never get out of this rut, and efforts to increase exports will themselves be undermined by persistent fiscal indiscipline, on top of a highly inefficient public sector. Which is why I insist that the first line of action in the current crisis is for the government to tackle what it has the most control over: Over-spending, by freezing employment, cutting back non-essential spending and eliminating waste. (More cocoa loans, Eurobonds, bridge loans, whatever loans, will at best provide temporary relief and enough room for multinationals to ship back the dollars as profits that they made in cedis.) These, plus serious short-, medium-, and long-term policies, including implementation of the 40-year plan, remain the surest way to rescuing the cedi and preserving its value, permanently.

Copyright © 1994 - 2026 GhanaWeb. All rights reserved.