President of Mpedigree, Bright Simons

President of Mpedigree, Bright Simons

So I checked into Facebook looking for something to sate my restless curiosity.

I got Menzbanc/Menzgold.

Not the most glamorous of subjects, but it will do.

The Bank of Ghana issued a statement warning, or is it notifying, the public not to make any cash deposits at Menzbanc as the company is not licensed to take deposits.

Menzbanc took a full page advert in the dailies to issue a rather bombastic "rebuttal" denying ever taking deposits.

So we have some kind of impasse. Rather typical of our "everything is debatable" culture in this country, no?

Whilst Menzgold's statement occasionally bordered on the hilarious, it also raised serious issues with the quality of financial sector regulation in Ghana.

What did Menzgold admit to doing?

Buying and selling gold as a "dealership".

So where does the "dividends" of 10% of principal a month it claims to pay come from?

A dealer makes a spread or a margin on trades. How then does a dealer pay dividends to anyone except its own shareholders?

This strange, Ghana-typical, mystery has to be solved by ignoring the plenty words adorning Menzgold's messianic statement in order to focus on the other essentials of its business model, as available on its website and elsewhere.

Menzgold encourages and facilitates the purchase of gold by its customers. It purports to own advanced bullion facilities that it operates at its cost. It stores the gold on behalf of its customers and export to other bullion facilities overseas (which presumably explains its partnership with an entity called "SwissGlobal").

How does this generate enough money to enable them pay a 10% return on investment that it calls "dividends" in order to avoid using the dreaded "interest" word? (interestingly, anti-usury schemes such as Islamic finance - sukuk - usually face similar terminological challenges).

Menzgold implies that it generates its investment income by leveraging gold price increases over the long-term. This time - based spread is then shared with the "gold depositor" in the form of a fixed monthly "dividend".

You don't have to be Warren Buffet to see that this is merely a crudely structured derivative.

To be more precise it is a rudimentary attempt to structure a commodity backed fixed income instrument, not all that dissimilar to the "commodity linked warrants" the Bank of Ghana claims it is interested in pushing in Ghana.

Which brings me to my first major point.

What in God's name is a central bank doing trying to regulate derivatives and exchange traded funds etc when we have a fully fledged Securities & Exchange Commission armed with a Security Industries Act, one as recent as 2016?

One whiff of the Menzgold broth and it should have been evident to BOG that the Dzorwulu based "gold dealer" has cooked its own asset backed security with a mind boggling fixed income yield structure and blended it with a Kovacs-style MLM strategy to pull in the dough from shortcuts-loving, profit hungry, hustlers.

Was it not immediately obvious to BOG that this is the SEC's terrain and that the latter now has the powers to adequately deal with any over the counter securities trader that isn't properly licensed to deal in securities? So why did they not refer the matter?

It looks like in the absence of a proper commodities futures regulator and given the fact of a meek securities regulator the BOG is intent on becoming an octopus, omnibus, financial sector supremo even in respect of matters for which it is not empowered by law or capacity to handle.

My point two is much shorter. If Menzgold describes its business as dealing in precious minerals and previous stones, and sells a financial product to the masses based on this underlying business model and asset base, then even before regulators move in, one would expect the financial press in a serious country to ask basic questions drawing on the wide body of information available on precious metals and stones business models.

No matter how you dice it a commodity - based derivative is limited by the general and historical price performance of the underlying asset.

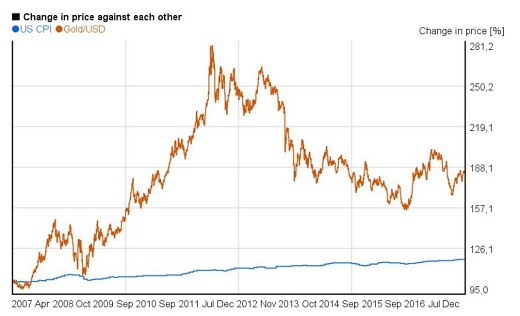

The real price of gold has never appreciated over the last century in a manner that suggests that it can power a 100% plus per annum return. In fact in real terms the value of gold has declined. A fact that lies at the base of the the old stereotype of gold being a "value store" rather than "income" play.

One only has to benchmark against the top global gold backed exchange traded funds, some of which have actually lost money in the last couple of years, to conclude that even a 10% annual return can be a real stretch. A perfectly understandable situation as real gold prices have dropped by about 30% since 2011 (see graph).

And if perchance Menzgold has invented a unique trading algorithm in a global market like gold, surely all the more reason we should be seeing intimately detailed investigative pieces from the financial press?

Copyright © 1994 - 2026 GhanaWeb. All rights reserved.